In today’s evolving wealth management landscape, the term “family office” has become synonymous with sophisticated portfolio and wealth management for high-net-worth families. But what exactly is a family office, and what should you look for when deciding whether one is right for you or your family’s financial affairs?

Understanding the Family Office Model

Families with significant wealth often have complex financial, legal, and estate considerations that go far beyond investment management. While traditional investment advisors typically focus on building and implementing portfolios, family offices provide a broader framework that integrates investment strategy with the family’s tax profile, estate planning, liquidity management, philanthropy, business succession, and long‑term family governance.

There are two primary models:

- Single-Family Office: Built for and by one ultra-affluent family; this structure manages all aspects of that family’s multi-generational financial and professional affairs.

- Multi-Family Office: Built to serve multiple affluent families; this structure delivers portfolio and wealth management services through a centralized team of professionals. Often also referred to as a “family office” in the Canadian marketplace.

While the concept of a single-family office may sound appealing by offering complete control, a dedicated staff, and personalized service, it’s important to understand the financial reality behind it. Establishing and maintaining a single-family office typically requires nine-figure wealth ($200 million or more). This is due to the high fixed costs of hiring a full-time team of investment professionals, financial planners, back-office support and administrative staff, along with the prerequisite technology and infrastructure to support them.

For most affluent individuals and families, this level of investment in a family office build out is neither practical nor cost efficient. Instead, the multi-family office model presents a more effective alternative by leveraging economies of scale. By pooling resources, a multi-family office can deliver comprehensive portfolio and wealth management services to multiple client families while still preserving the personalization, confidentiality, and white glove service that define a true family office experience. Critically, these teams also function as a central point of coordination, working with a family’s accountants, lawyers, and insurance professionals to align advice, manage complexity, and ensure that all deliverables are executed cohesively.

Not all multi-family offices are built the same. Whether you’re an individual seeking tailored financial advice or stewarding multi-generational wealth, choosing the right family office requires more than just evaluating investment performance. It’s about finding a partner whose philosophy, approach, and structure align with your values, can service the complexity of your wealth, and support the realization of your long-term vision.

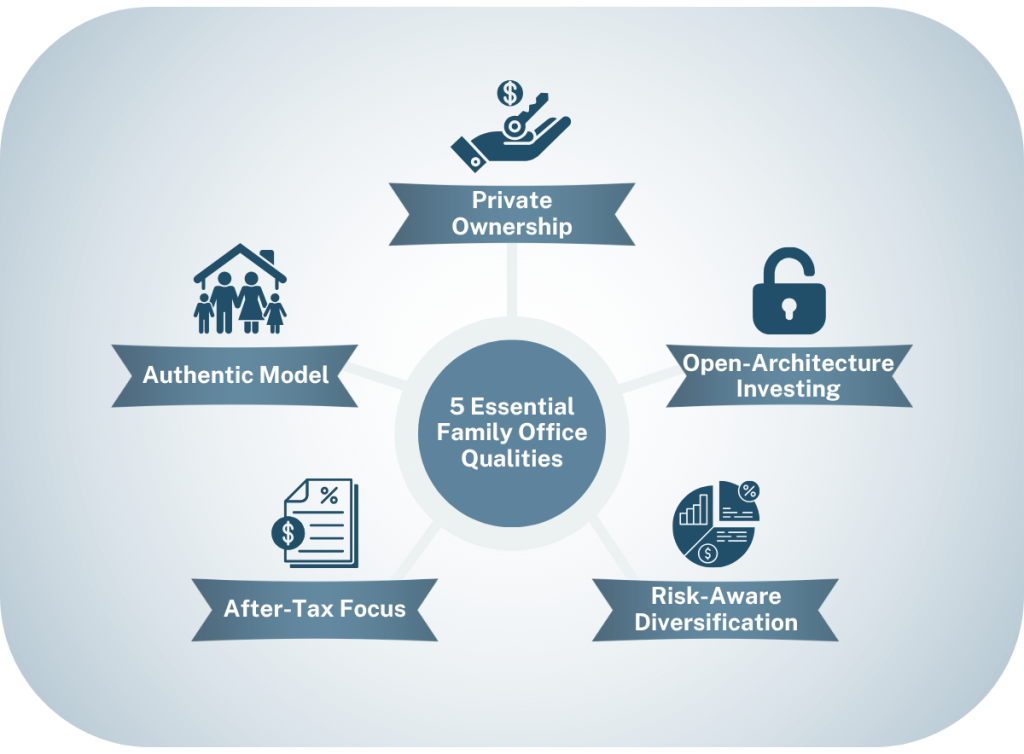

Here are five essential qualities to look for when evaluating a multi-family office:

1. Private Ownership with a Singular Focus on Clients

Publicly owned multi-family offices operate under the dual mandate of serving clients and satisfying shareholder expectations. While large public family offices may enjoy deeper coffers and greater brand equity, public ownership can introduce competing priorities that influence decision-making. What’s best for the shareholders may not be best for the family office clients. By contrast, privately held family offices are free from this dual mandate, allowing them to focus exclusively on client outcomes while fostering long-term relationships with multiple family generations.

2. An Authentic Family Office Model

Many asset management firms have launched family office offerings to capitalize on market demand and cache. These family offices typically offer standardized investment services under a premium label, but at their core they remain commercial enterprises driven by scale and profitability. An authentic family office, by contrast, has an active founding family that invests alongside other clients. This structure creates stronger alignment, as investment decisions are shaped by shared objectives rather than corporate priorities. Cornerstone founding families have often navigated similar situations their affluent clients encounter allowing for fuller context and counsel.

3. Open-Architecture Investing

Family offices with closed architecture often restrict investment options to proprietary products and a rigid set of strategies, which can restrict diversification and lead to sub-optimal investment outcomes. Family offices practicing open architecture investing can access the full universe of public and private investment opportunities, including hedge funds, private equity, private real estate, and specialty fund vehicles. Investment opportunities are then judged solely on their merit and implemented for a client only if it suits their investment goals and risk profile. Again, the client can take comfort knowing the cornerstone founding family owns the same investments on the same terms as clients. This flexibility is the foundation of open‑architecture investing, enabling families to pursue the best opportunities without being restricted to in-house offerings and pre-packaged strategies.

4. An After-Tax Focus

Many family offices emphasize pre-tax returns, often overlooking the significant impact of taxes on wealth preservation. A family office practicing tax-conscious investing means that its portfolio managers focus on enhancing after-tax returns in every investment decision by optimizing for net outcomes rather than headline pre-tax return numbers. This approach ensures that family wealth is managed with a view toward real-world results and long-term capital planning.

5. Risk-Aware Diversification

While some family offices develop deep expertise in specific asset classes, such as real estate or private credit, excessive concentration can heighten risk when a single sector faces cyclical or structural pressures. Family offices that adequately size different exposures in their clients’ portfolios help to ensure that challenges in any one area do not disproportionately affect overall portfolio outcomes. This disciplined approach enables portfolios to remain resilient through market stress while retaining flexibility through changing market conditions.

Selecting a family office is ultimately about trust, alignment, and capability. For families navigating increasing financial complexity, the right partner brings clarity, coordination, and long-term wealth stewardship across generations. If you are exploring whether a family office is appropriate for you or your family’s circumstances, we would be happy to discuss your wealth objectives. Get in touch with a senior portfolio manager here.