One of the most important discoveries in finance over the past few decades is that stocks of firms that share certain fundamental characteristics called “factors” exhibit different return and risk characteristics than the overall market. Critical to investors is the fact that, over long periods of time, certain of these factors have earned excess returns compared to the overall market.

Broadly speaking, these factors can be distilled into the following categories:

- Value: Stocks that are low-priced in relation to earnings, dividends, cash flow or book value, on average, have outperformed growth stocks over long time horizons.

- Size: Stocks of small and mid-size companies have earned, on average, higher returns than stocks of large companies over long time periods.

- Momentum: Stocks that have exhibited positive momentum – i.e., have performed relatively well over the past 3 to 12 months – have outperformed, on average, over long time horizons stocks that display negative momentum.

- High Yield: Stocks of companies that pay higher dividends, on average, have earned superior returns to lower and non-dividend paying stocks over the long run.

- Quality: Stocks that have evidenced superior profitability in relation to capital have, on average, outperformed firms with poorer profitability in relation to capital over long time horizons.

- Low Volatility: Stocks that have exhibited low volatility have, on average, outperformed stocks that display high volatility over the long run.

There are two primary explanations for the higher returns associated with these factors. One is that the higher returns represent risk premiums – i.e. compensation to investors for incremental risks beyond that of the total stock market. For example, small company stocks are not only more volatile than stocks of large companies but are also much less liquid. Value stocks tend to include a higher proportion of heavily indebted companies which dramatically underperform the overall market during periods of extreme market stress.

The second explanation is offered by behavioural finance. Investors’ cognitive biases such as “myopia” and “overconfidence” can lead to the persistent mispricing of certain securities. For example, many investors are attracted to the episodic outsized returns of high volatility, low quality stocks and chase these types of stocks despite a pattern of longer-term underperformance. Overly optimistic investors overestimate the earnings prospects of growth stocks while underestimating those of value stocks; value stocks then generate superior returns as investors eventually realize that earnings in the value universe are better than initially expected. The “herding” behaviour of investors has been advanced as an explanation for the returns associated with the momentum factor.

Social phenomena such as the “bandwagon effect” can also distort prices. The “madness of crowds” – as evidenced by the railway mania of the 1840’s, the Florida real estate boom of the 1920’s, the Japanese bubble of the 1980’s and the internet mania of the 1990’s – is a well-documented recurring market spectacle. Investors’ infatuation with extremely expensive US growth names these last several years will likely be added to the textbooks as the most recent example.

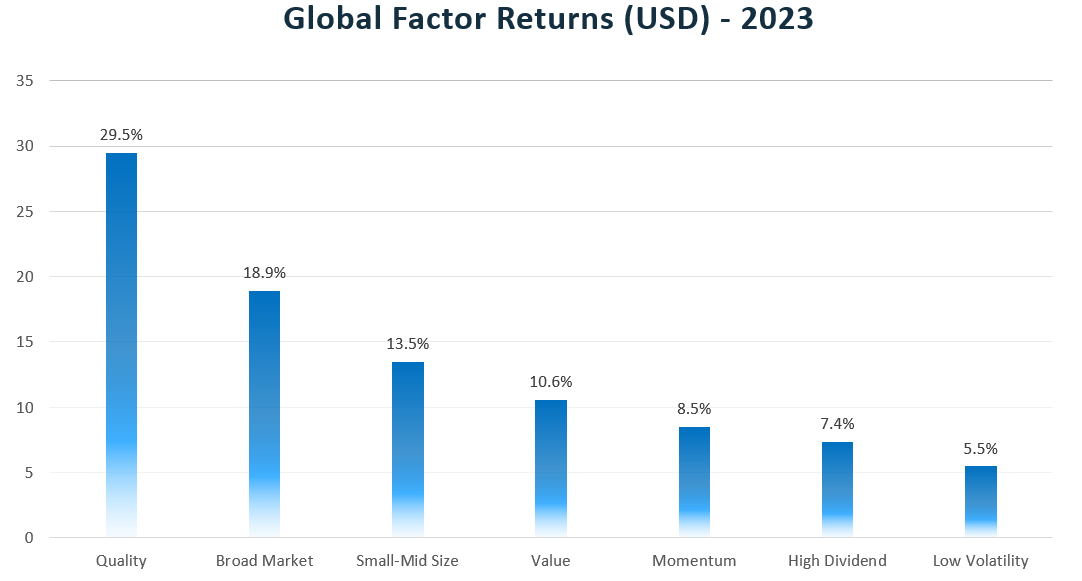

Factor performance can vary because of business cycle influences, market sentiment, interest rate changes, sector composition and other variables. The following chart sets out the return earned by each factor globally in 2023 compared to the overall broad market. (See Appendix I for Sources).

Quality stocks came in first on relative factor performance with a whopping 29.5% return in 2023. Quality’s blistering return can be chiefly attributed to the resounding gains made by US technology mega-cap stocks that rode a wave of AI fervour throughout the year. 2023’s performance marked a full reversal of the dismal returns from just one year earlier – quality suffered the worst factor loss of 2022 at -23.4%. Broad market stocks followed quality in 2023 with a strong performance of 18.9% on the year. Small-mid size stocks also faired well, though not as well as the broad market, posting 13.5%. Value, momentum and high dividend stocks followed with decreasing positive returns. Finally, low volatility brought up the rear for 2023 posting a middling return of just 5.5% versus the broad market.

While the outperformance of any one factor in any given year is unpredictable (making “factor timing” a mug’s game) diversifying across factors and systematically rebalancing allocations can augment portfolio returns over time. As illustrated by the following graph depicting the cumulative growth of $100 USD invested since 2000, the global multi-factor portfolio has created an incredible 43% more wealth than the global broad market index (see Appendix I for the indexes used and disclaimer).

Twenty years ago, “factors” were a fascinating corner of the capital markets but of little practical use to individual investors. Since then, with the advent of low-cost exchange traded funds and the creation of transparent, rules-based factor indices by a range of index providers, a multi-factor portfolio has moved from academic theory to concrete application. Patient investors finally have an empirically sound approach to pursuing market-beating returns.

Appendix

| Global Factor/Portfolio/Market | Index (USD) |

| High Dividend Yield | MSCI ACWI High Dividend Yield |

| Low Volatility | MSCI ACWI Global Minimum Volatility |

| Momentum | MSCI ACWI Momentum |

| Quality | MSCI ACWI Quality |

| Size | MSCI ACWI SMID Cap Index |

| Value | 50% MSCI ACWI Large Cap Value

50% MSCI ACWI SMID Value |

| Global Multi-Factor | Equal Weight of the Above 6 Factors;

Rebalanced Monthly |

| Broad Market | MSCI ACWI Investable Market Index |

Disclaimer

Tacita Capital Inc. (“Tacita”) is a private, independent family office and investment counselling firm that specializes in providing integrated wealth advisory and portfolio management services.

Tacita research has been prepared without regard to the financial circumstances and objectives of any individual investor. The asset classes/securities/instruments/strategies discussed may not be suitable for all investors and certain investors may not be eligible to purchase or participate in some or all of them. It is not possible to invest directly in an index. Whether a particular investment or strategy is appropriate depends on individual circumstances and objectives. Investors should therefore independently evaluate particular investments and strategies or seek the advice of a financial advisor.

All investments involve risk including loss of principal. Past performance is not necessarily a guide to future performance; estimates of future performance are based on assumptions that may not be realized. Management fees and expenses are associated with investing.

Tacita research is based on public information and is prepared for informational purposes. While we make every effort to use reliable, comprehensive information, we do not warrant that it is accurate or complete. We assume no obligation to inform anyone should the opinions, estimates or information provided change.

Tacita research is not intended to provide tax, legal, or accounting advice. Investors should obtain their own professional advice in this regard.

Neither the information provided nor any opinion expressed in our research constitutes a solicitation by Tacita for the purchase or sale of any securities or financial products.